India’s industrial economy is growing steadily year-on-year, supported by higher capital expenditure in the Union Budget 2026–27, with allocations rising by 11.5% (USD 131 billion to 148 billion). Meanwhile, the transition from the Perform, Achieve and Trade (PAT) scheme to the Carbon Credit Trading Scheme (CCTS), while often seen as a regulatory evolution, signals a deeper structural shift.

As the EU’s CBAM begins imposing carbon-linked import tariffs, a key question emerges: is India’s domestic carbon market ready?

At its core, readiness is about market design and whether companies can measure, price, and act on carbon as a business variable.

CCTS is India’s emerging cap-and-trade mechanism that sets emissions intensity targets for industrial entities and enables the trading of carbon credit certificates within a regulated market. This transition matters less for its immediate price impact, and more for how it reshapes carbon from a reporting metric into a financial and strategic variable.

Carbon becoming material is not a question of if, but when, and how quickly.

What PAT Achieved, and Where It Fell Short

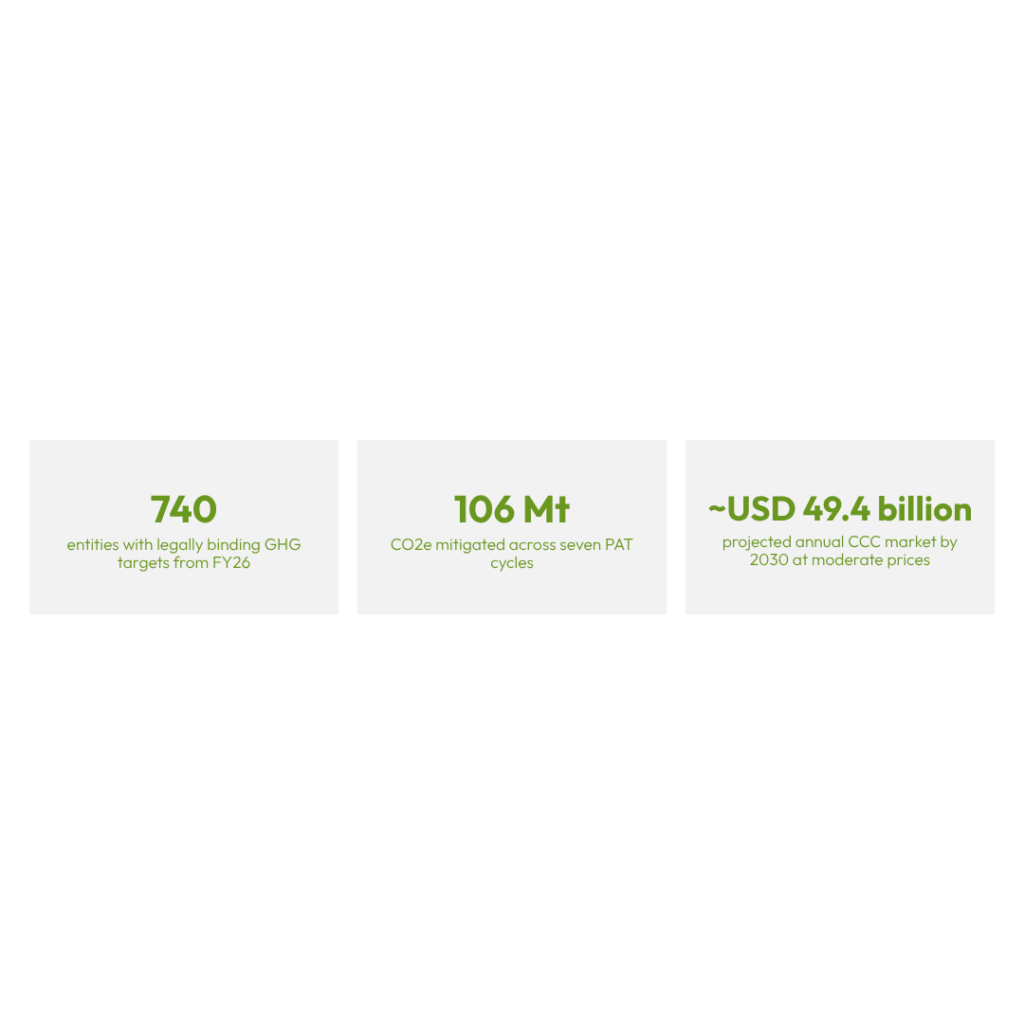

The PAT scheme, in place since 2012, demonstrated that market-based mechanisms can drive energy efficiency at scale. Across successive PAT cycles, India Inc. has abated over 106 million tonnes of CO₂ emissions. The country also became a leading participant in global carbon markets, with the second-highest number of Clean Development Mechanism (CDM) projects.

Companies such as UltraTech Cement and Hindalco built capabilities in emissions accounting and credit trading ahead of regulatory mandates, creating a strong foundation for CCTS.

However, PAT was built around energy intensity, rather than emissions. The implied carbon price in its trading certificates remained below USD 7 per tonne, far lower than the USD 60 to USD 80 range in the European Union Emissions Trading System. A significant share of required certificates remained unpurchased, with limited consequences for non-compliance. As a result, PAT rarely created a cost material enough for finance functions to prioritise.

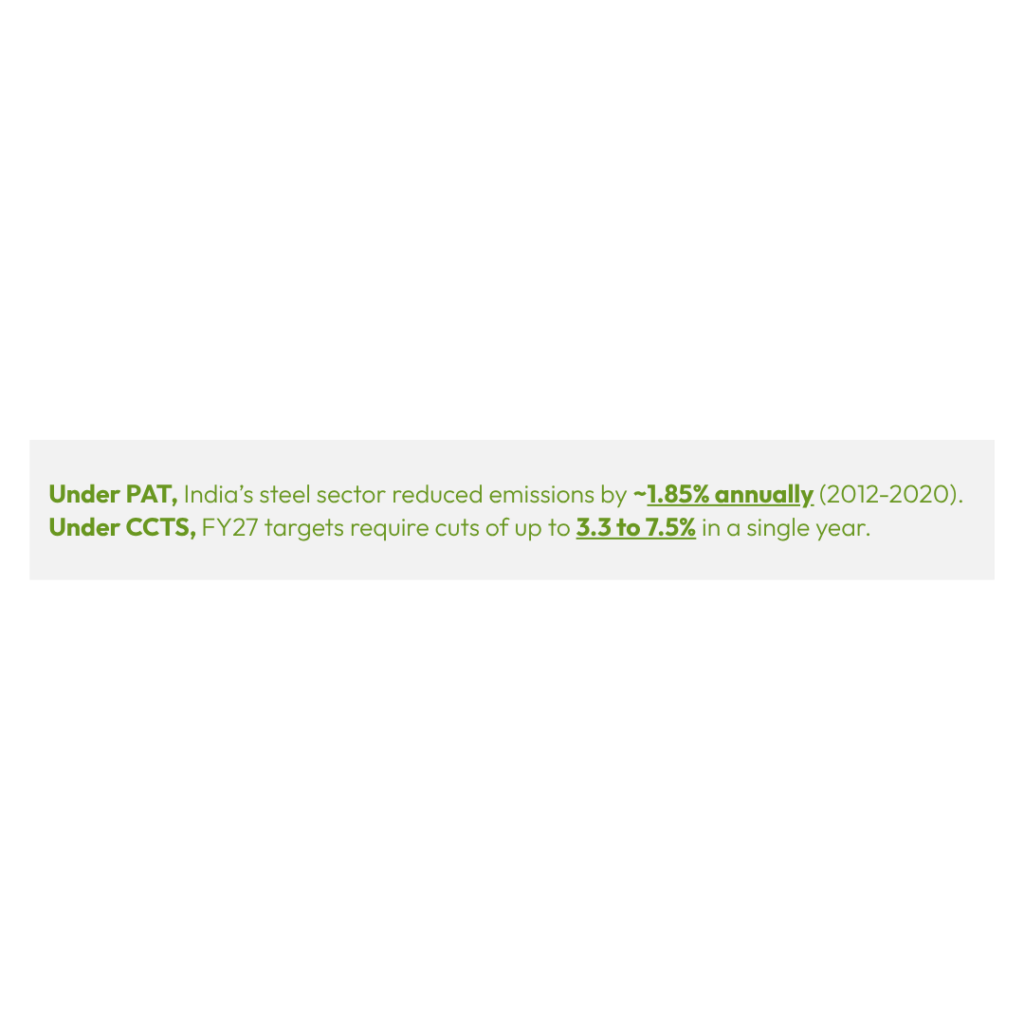

CCTS is designed to change that. It defines targets in terms of emissions (tCO₂e per unit of output); with non-compliance carrying penalties at twice the prevailing credit price. Phase 1 starts with 1-3% reductions in FY26, rising to 2-8% in FY27, with further tightening thereafter. Coverage begins with nine sectors and is expected to expand to 26–27 sectors.

The shift is structural: from efficiency-led optimisation to emissions-linked accountability, with clearer financial consequences.

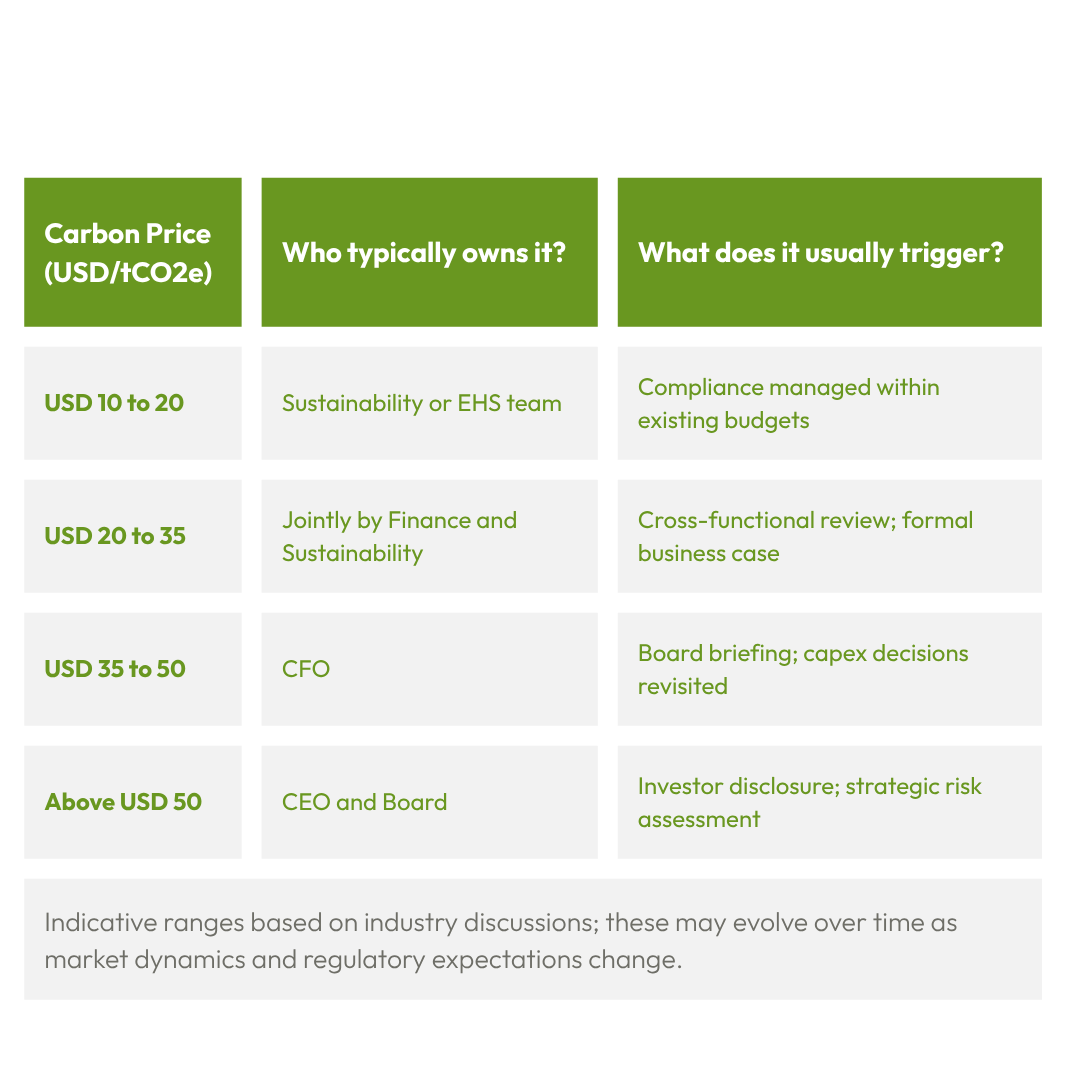

When Does Carbon Become a Financial Priority?

Carbon shifts from a sustainability concern to a financial one when pricing becomes material. A consistent pattern emerges across industries:

India’s compliance market is expected to open at USD10-USD15 per tonne, placing it firmly in the first category. In the near term, CCTS compliance may sit within existing sustainability structures.

Yet, even at modest price levels, the impact is non-trivial for emissions-intensive sectors, especially where carbon costs intersect with energy prices, export exposure, and supply chain pressures.

More importantly, external signals are already accelerating this shift. The EU’s Carbon Border Adjustment Mechanism entered its financial phase in January 2026. Indian steel exporters face an estimated USD 2 billion exposure by 2030, with potential levies reaching USD 397 per tonne by 2034 without credible abatement.

These costs are already influencing commercial negotiations between Indian exporters and European buyers, well before domestic prices fully reflect them.

How the Challenge Differs Across Sectors

CCTS applies a common compliance framework across sectors, but decarbonisation pathways vary widely.

In hard-to-abate sectors like cement and steel, emissions reduction requires capital-intensive, long-horizon technologies. Most efficiency gains have already been captured, while solutions such as carbon capture, green hydrogen, and alternative chemistries require sustained investment and policy support, beyond what carbon markets alone can justify.

As a result, leading companies are responding to carbon trajectory and export competitiveness, not just current prices.

- UltraTech Cement is targeting 85% renewable energy by 2030, investing in captive solar, and piloting carbon capture to build long-term cost stability and carbon resilience.

- Tata Steel has created India’s first Carbon Bank, structuring verified CO₂ reductions to enable low-carbon steel offerings.

- JSW Steel has raised USD500 million through sustainability-linked bonds and committed USD1 billion to decarbonisation.

- Hindalco has launched 100 MW round-the-clock renewable hybrid pilots for its aluminium smelters in FY24, combining solar, wind, and battery storage to ensure uninterrupted industrial power at scale.

In knowledge-economy sectors, the shift is more embedded. Tech Mahindra has SBTi-approved net-zero targets for FY2035 and uses an internal carbon pricing mechanism to evaluate capital allocation. Across sectors, companies are integrating carbon into decision-making ahead of regulation catching up.

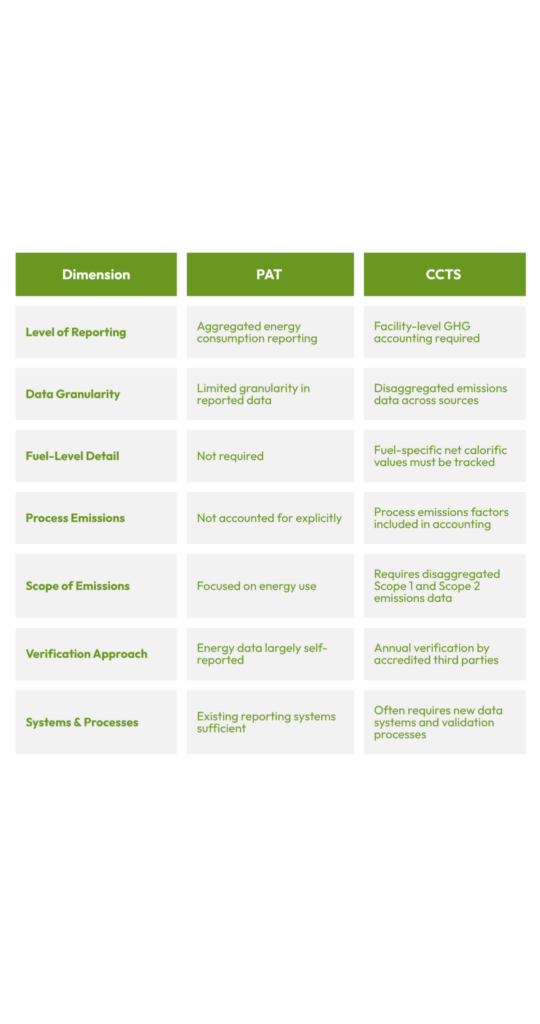

The Measurement Gap Most Organisations Underestimated

The shift from PAT to CCTS requires a fundamental upgrade in how emissions are measured and verified. The comparison below highlights how reporting expectations are becoming more granular, rigorous, and audit-driven:

For many organisations, the gap between current systems and CCTS requirements is substantial. A useful parallel is India’s Ind AS transition. Companies that invested early in rebuilding systems and audit relationships navigated it with ease, while those that treated it as a deadline-driven exercise, faced higher costs and complexities.

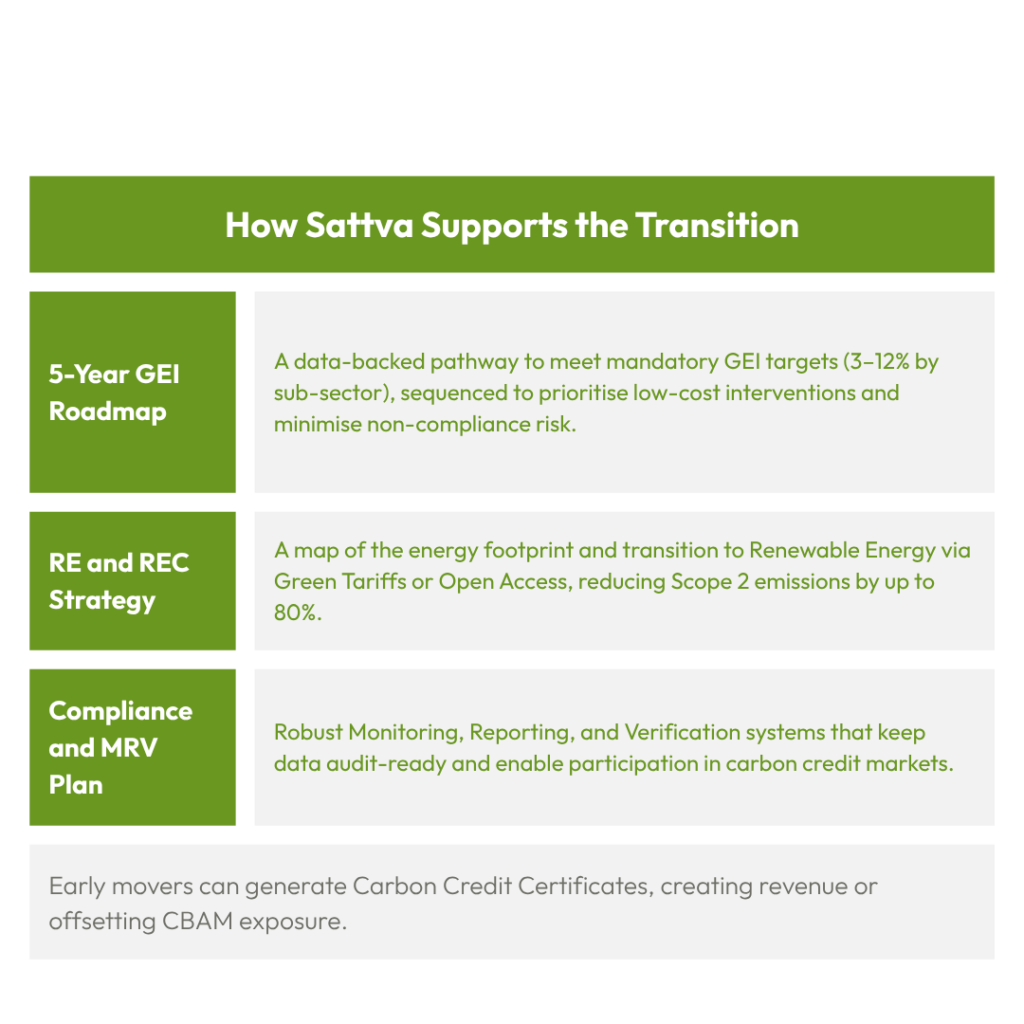

Under CCTS, preparation costs scale linearly, but delays compound non-linearly. Companies with audit-ready MRV systems will be better positioned to generate credible Carbon Credit Certificates, access green financing, and meet CBAM-related documentation requirements from global buyers.

Where Organisations are Finding Traction

Many organisations still treat CCTS as compliance, delaying MRV investments and underestimating timelines, increasing cost and execution risk.

In contrast, leading organisations are making early, deliberate moves by:

- Establishing verified, facility-level emissions baselines

- Developing renewable energy strategies to address Scope 2 emissions

- Embedding internal carbon pricing into capital allocation

- Shifting carbon accountability to the CFO, not just sustainability teams

Companies such as UltraTech, Tata Steel, JSW Steel, Hindalco, Tech Mahindra, and Mahindra Group illustrate what early, deliberate action looks like.

The CCTS compliance cycle begins in FY26. CBAM is already in effect, and carbon markets are expected to be operational by late 2026, creating a narrow but critical window.

Organisations that use this period to establish baselines, build measurement systems, and define credible abatement pathways will retain strategic flexibility as targets tighten. Those that delay risk higher compliance costs, limited market access, and reactive capital allocation.

This transition will redefine industrial competitiveness in a carbon-constrained world. If you are assessing how CCTS will impact your business, or how to move from compliance to competitive advantage, write to us at esg@sattva.co.in. We would be glad to exchange perspectives.

All views expressed are personal.