Sattva Consulting and India Data Insights analysed 98 manufacturing companies across 15 industries, collectively accounting for approximately ₹13,680 crore in CSR spending between FY2021-22 and FY2023-24. The study shows a geographic shift in the deployment of CSR capital. These firms operate more than 750 manufacturing facilities across 289 districts in India, anchoring CSR decisions closely to their operational footprint.

Firms investing locally outspend CSR mandates

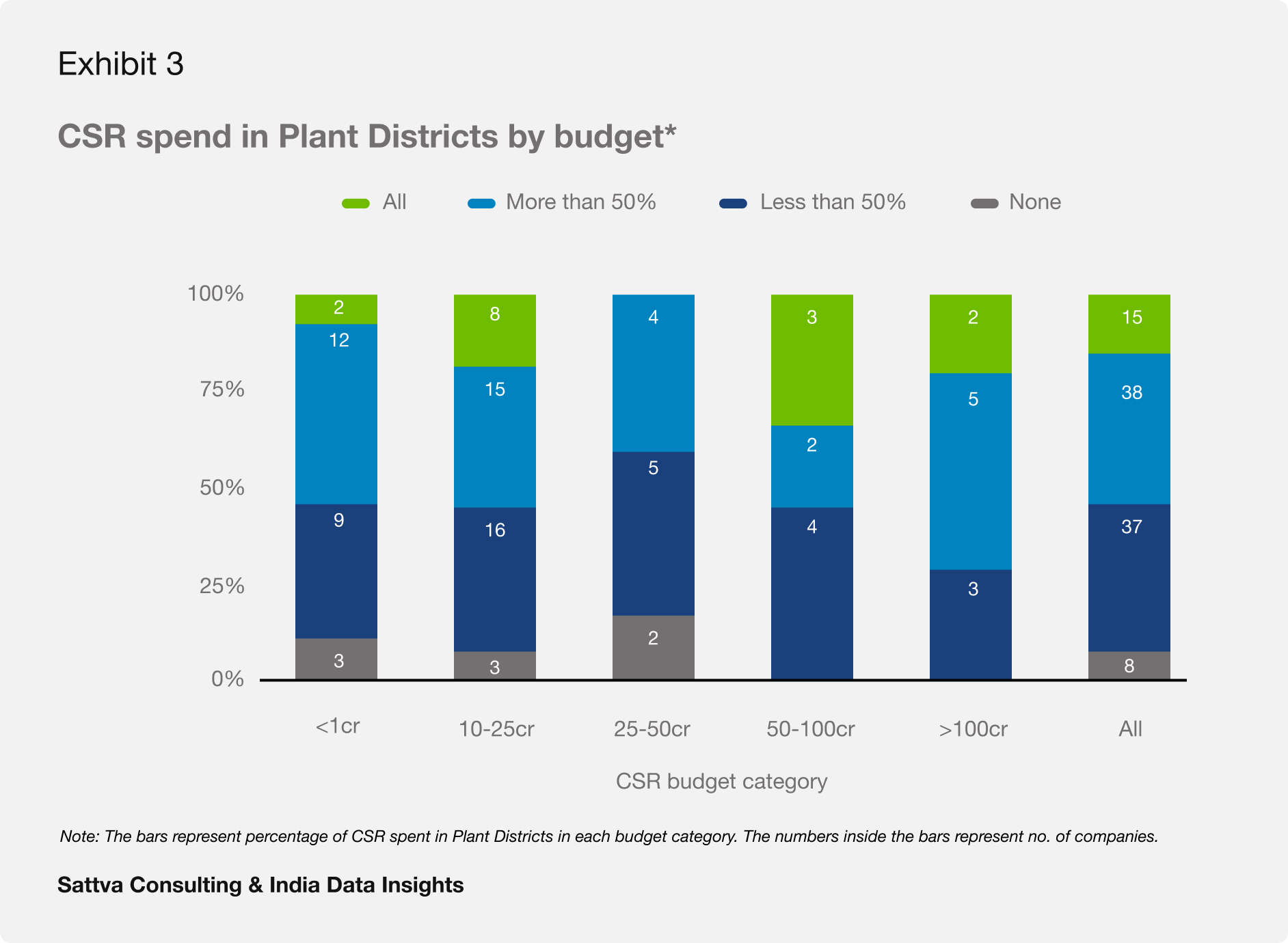

Companies with a higher share of CSR spending in plant districts are more likely to exceed statutory requirements. Around 51% of such firms spend at least 50% more than their mandated CSR obligation, indicating that locally anchored strategies often go beyond compliance thresholds.

This suggests that proximity to operations may influence both governance and spending behaviour, with companies leveraging their physical presence to drive deeper engagement and oversight.

Industry type drives where CSR flows

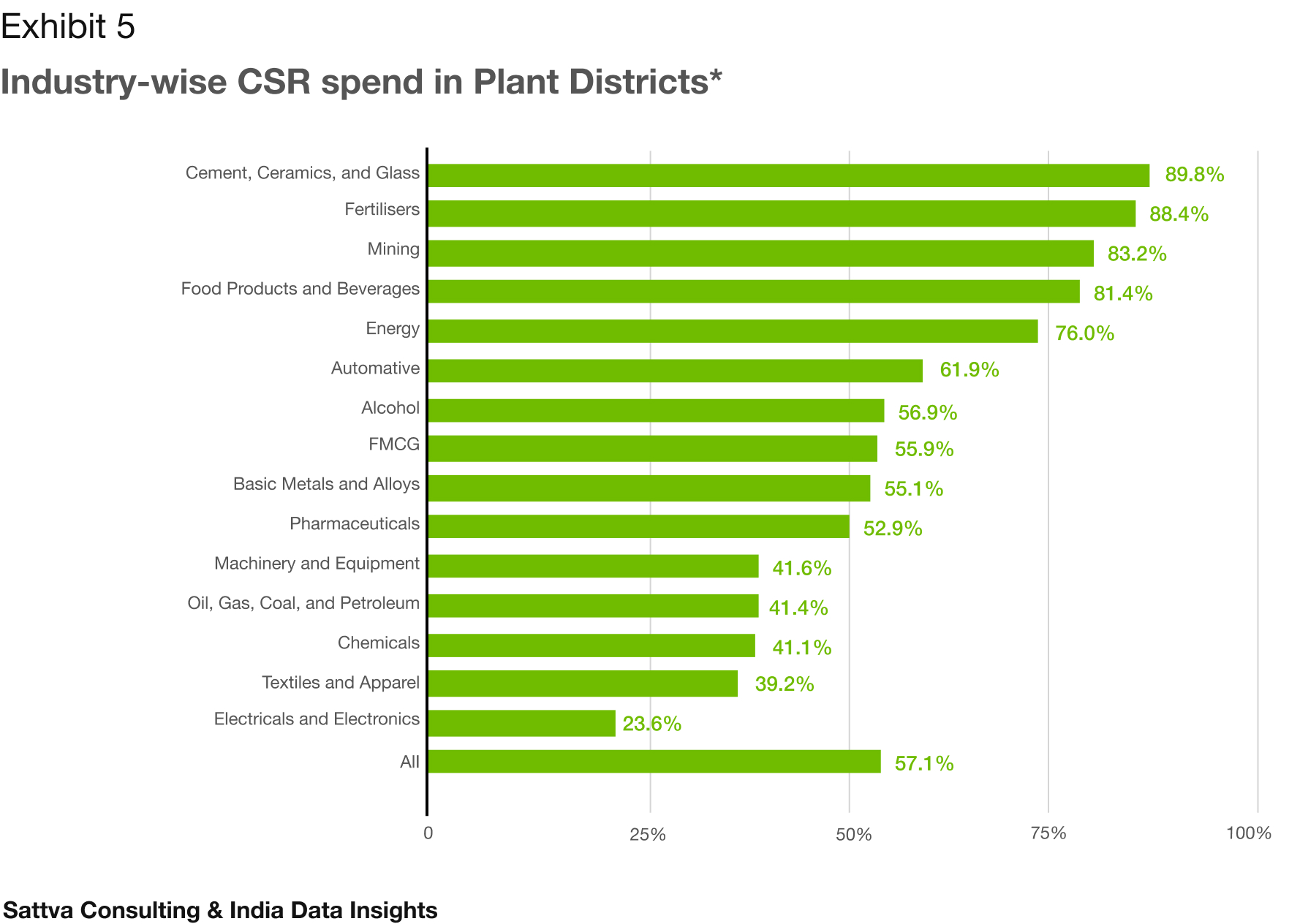

The degree of localisation varies significantly by industry. In extraction-heavy sectors such as mining, energy, and cement, more than 70% of CSR spending is concentrated in plant districts, reflecting the need to mitigate environmental and social risks and maintain community trust.

In contrast, sectors such as electronics, chemicals, and textiles allocate less than half of their CSR budgets locally, indicating lower dependence on specific geographies. Consumer-facing sectors, including automotive, alcohol, and FMCG, cluster around the average, close to 57%, suggesting a hybrid approach that balances local investments with broader national initiatives.

Overall, geographic concentration ranges widely, from around 20% to over 80%, underscoring the role of operational intensity in shaping CSR strategy.

Few sectors and projects capture the bulk of plant-level CSR

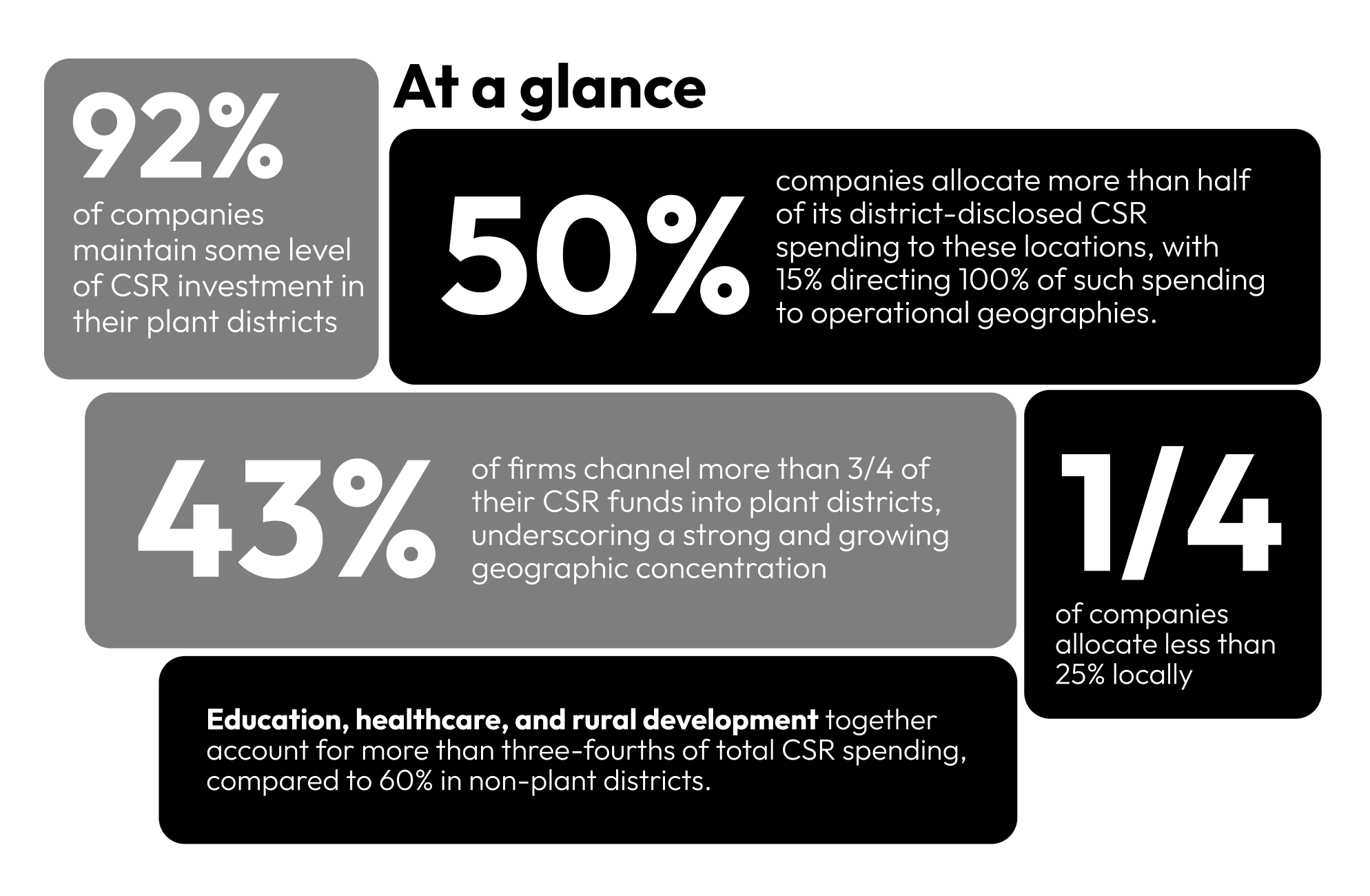

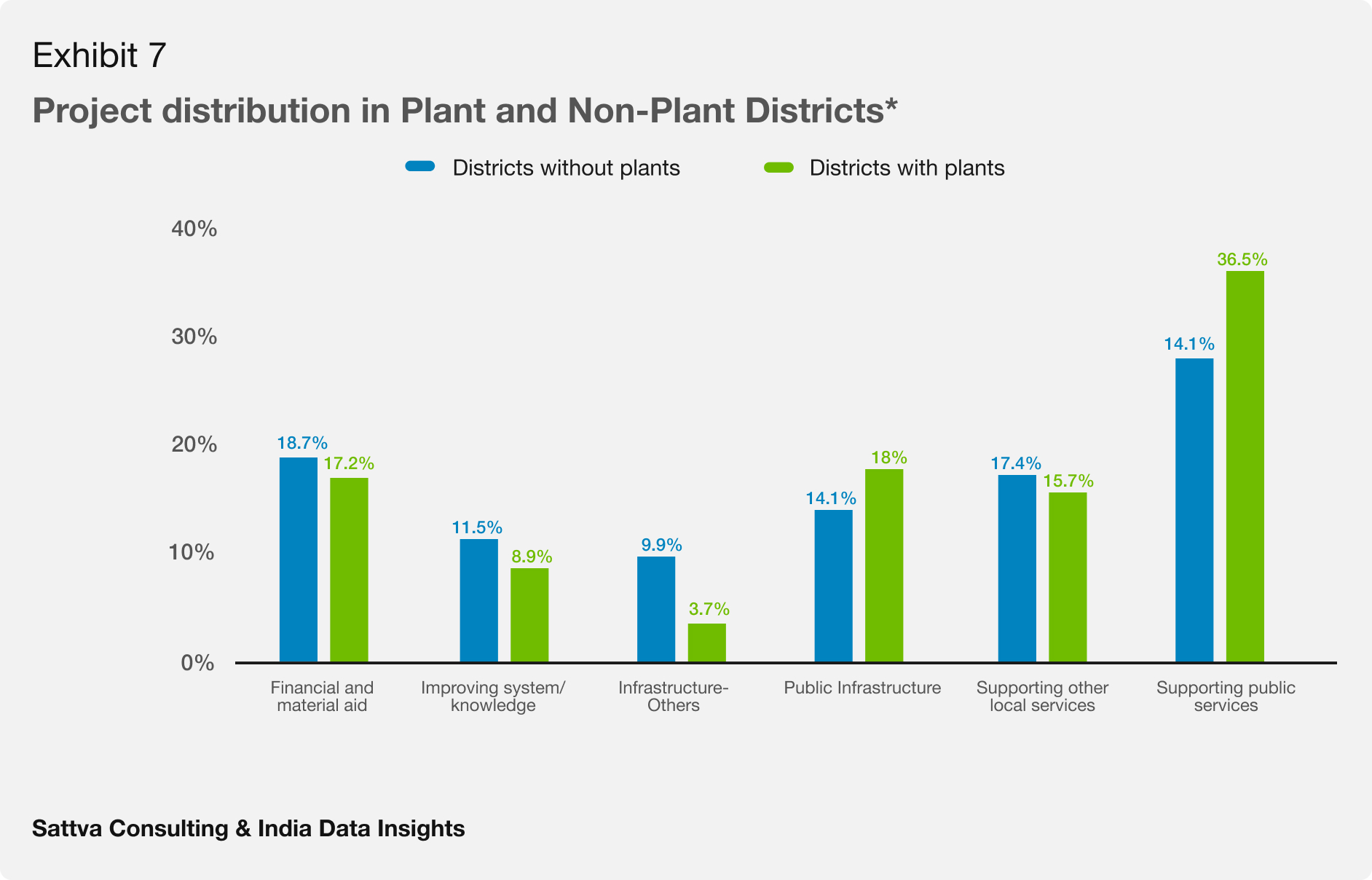

Within plant districts, CSR spending is heavily skewed toward a few sectors. Education, healthcare, and rural development together account for more than three-fourths of total CSR spending, compared to 60% in non-plant districts.

By contrast, livelihood development and environmental initiatives receive a relatively larger share in non-plant districts, roughly double that in plant locations. Even within livelihoods, the focus remains narrow; vocational skills account for just 4% of spending in plant districts, compared to 2.8% elsewhere, indicating a modest emphasis on workforce upskilling.

Analysis of 6,455 projects shows that 26% of infrastructure funding in plant districts is directed toward just six large rural development projects. In service-oriented categories, healthcare accounts for 31% of spending and education 28%, together making up nearly three-fifths of such investments.

Overall, 57% of district-disclosed CSR spending and 35% of total CSR spending is concentrated in plant districts, confirming geographic alignment as a defining feature of manufacturing CSR.

Companies are directing capital to regions where they maintain long-term production assets, reflecting the interdependence between industry and local communities. However, the data also highlights a concentration challenge. While CSR is geographically aligned, it remains clustered in visible, service-oriented sectors, with relatively lower investment in long-term economic and environmental resilience.

As this trend deepens, the opportunity lies in evolving from proximity-driven spending to more integrated, place-based strategies. With 289 plant districts represented in the dataset, these regions function not just as production centres but as interconnected systems of livelihoods, public services, and natural resources.