ESG in India’s insurance sector is increasingly shaped by regulatory momentum and the need to align with global standards. Insurers are now expected to embed ESG across underwriting, investments, operations, and product innovation, not just disclose it. However, India is still in the early stages of the ESG journey, with most efforts centred around compliance and limited risk management rather than full integration across the value chain.

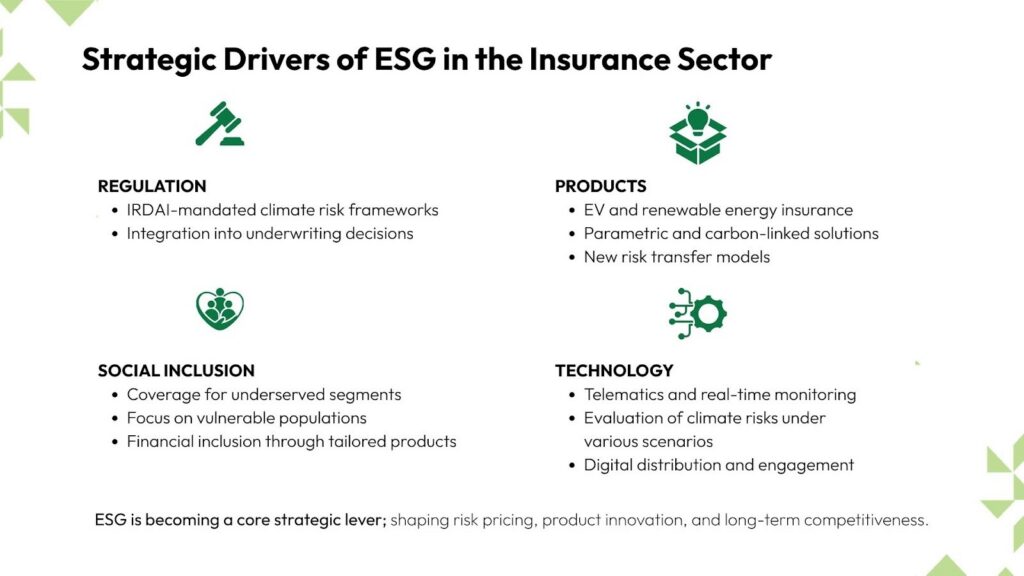

Regulatory Drivers of ESG in the Insurance Sector

The Business Responsibility and Sustainability Report (BRSR) mandates that listed insurers disclose environmental metrics, such as energy use, water consumption, emissions, and waste management, alongside social and governance indicators, including human rights, labour practices, diversity, and community engagement. However, BRSR currently covers only 11 out of the 59 insurance companies registered by the Insurance Regulatory and Development Authority of India (IRDAI), limiting its sector-wide impact.

A 2024 circular from IRDAI signals a move towards system-wide ESG integration. Insurers need to adopt board-approved ESG frameworks and to monitor performance, marking a transition from disclosure-led compliance to institutional accountability.

Further, the proposed adoption of Indian Accounting Standards (Ind AS) from 2026 is expected to align the sector more closely with global IFRS norms. This transition improves transparency in risk assessment, liability valuation, and investment performance; areas increasingly shaped by ESG considerations. Recent governance regulations reinforce this direction by explicitly placing ESG responsibility at the board level.

Beyond domestic regulation, global developments are accelerating ESG adoption. A significant number of Indian insurers operate as joint ventures with international partners, primarily from Europe (17 JVs), followed by Japan (7), the US (3), Australia (2), and Canada (2). These markets are converging towards ISSB standards (IFRS S1 and S2), along with region-specific mandates, creating a strong push for alignment across Indian entities.

Key Challenges in ESG Integration

Despite growing momentum, ESG integration remains uneven, with insurers facing structural barriers across people, processes, and data systems.

On the people front, challenges include uneven stakeholder buy-in, limited internal accountability due to unclear roles and incentives, and the continued perception of ESG as a compliance exercise rather than a strategic priority. However, in reality, there is a knowledge gap in employee awareness about various facets of ESG and how it interacts with their day-to-day roles and decisions.

Process-related barriers are also observed in embedding ESG into underwriting and investment decisions, and the absence of standardised exclusion frameworks. Insurers must also navigate trade-offs between financial returns and ESG objectives, compounded by a limited pool of ESG-aligned investment assets in India.

ESG data is often fragmented across legacy systems, with high costs associated with system upgrades and integration. Traditional actuarial models are not yet equipped to fully capture region-specific climate risks, limiting the integration of forward-looking ESG insights in decision-making.

The Next Step in the ESG Journey

However, it’s the underwriting, investment, and compliance functions that sit at the forefront of execution:

- Underwriting teams are starting to incorporate ESG considerations into risk assessment and pricing. While most insurers in India now offer EV insurance products, some players are moving further along the curve. For example, HDFC ERGO and Zuno General Insurance provide additional EV-specific add-ons, including coverage for home charging infrastructure, charging-related electrical risks such as short circuits, and associated accessories. In parallel, innovation is also emerging through parametric insurance solutions, with insurers such as New India Assurance and Go Digit General Assurance piloting index-based products that trigger payouts based on predefined climate parameters, signalling a broader evolution in underwriting approaches toward climate risk responsiveness.

- Investment teams are embedding ESG into portfolio strategies through risk screening, climate scenario analysis (for example: ICICI Prudential Life Insurance), and alignment with global frameworks such as PRI, while navigating a developing pool of ESG-aligned assets in India.

- Compliance teams anchor ESG data collection, validation, disclosures, and regulatory reporting, particularly as expectations from IRDAI and global investors evolve.

For ESG to become operational, integration must extend across the organisation:

- Human resources has to build internal capability through ESG training, integrate ESG into performance management, and strengthen accountability across teams.

- Product teams need to incorporate ESG into product design, including EV-linked insurance, climate risk covers, and inclusive insurance offerings for underserved segments.

- Marketing and distribution teams should translate ESG efforts into customer engagement, positioning, and differentiated value propositions.

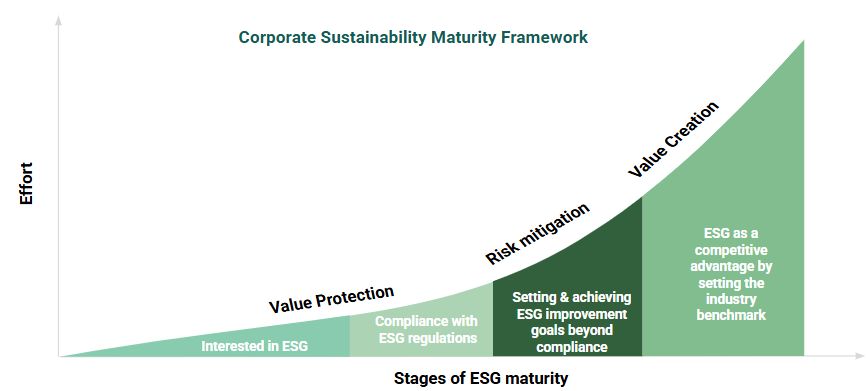

Early signs of these shifts are already visible in the country. Most insurers in India have begun strengthening ESG disclosures, integrating climate considerations, and expanding product offerings aligned with emerging risks. While still evolving, these efforts point to a clear direction: ESG is moving beyond reporting to become a cross-functional driver of decision-making. Organisations that operationalise it early will be better able to manage risk and capitalise on emerging opportunities.

ESG is beginning to influence underwriting, investments, and regulatory expectations in India’s insurance sector. However, its impact still depends on how it translates into day-to-day decisions. A more consistent approach involves regularly reviewing material risks through inputs from diverse stakeholders, as climate risks, regulatory expectations, and market dynamics continue to evolve in India.

Equally important is strengthening internal capacity to translate ESG frameworks into day-to-day actions. Often, ESG stays at the policy level, with limited linkage to underwriting, actuarial, and investment decisions. So, strengthening role-specific capability, improving data systems, and risk models can help bridge this gap.

Over time, insurers that actively review their material risks and invest in internal capability are better positioned to manage emerging risks and identify opportunities as ESG expectations deepen. If you’re an organisation navigating ESG integration, materiality, or capacity building, write to us at esg@sattva.co.in.

This piece is authored by Vrinda Gupta, Engagement Manager, Sustainability and Business Advisory. All views expressed are personal.