Sahana Lakshmi

Sustainability Reporting in India: An evolution

Sustainability focus in business is no longer optional. Climate change, environmental impact, social disruptions, and governance inefficiencies have strongly influenced stakeholder views of corporate resilience and adaptation in the past decade. An interplay between pull (competitive advantage, investor interest) and push factors (stakeholder demand, regulatory compliance) is actively contributing to the need for corporates to strategise, measure, disclose and improve indicators of Environment, Social and Governance (ESG) sustainability.

Consequently, the ESG reporting and disclosure landscape has witnessed significant change globally. Within two decades, there has been emergence of various voluntary reporting frameworks and standards that have attempted to pave the way for standardized reporting. However, corporate adoption has been a challenge due to the volume and variance within ESG standards and their voluntary nature of implementation.

After decades of voluntary engagement, regulators are taking the reins in both developed and emerging countries to increasingly adopt mandatory paths to enforce transparency. This is a significant first step towards substantive shifts in performance to meet ambitious national targets for a sustainable future. There has been a 2x increase in global capital market ESG regulations between 2000-2021 with the APAC region seeing a 2x increase in the latter half of this period*.

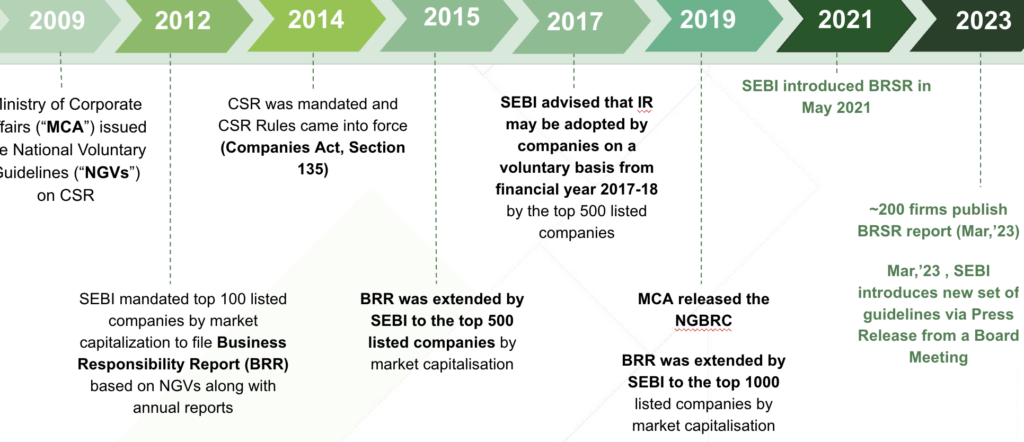

Indian regulators, particularly SEBI, have been leading the push dynamic by taking a progressive or ‘glide path’ to ESG integration over the last decade. The introduction of the mandated and comprehensive Business Responsibility and Sustainability reporting (BRSR) for the top 1000 companies by market capitalisation has been a milestone regulation that was expected to drive ESG integration among Indian companies.

Evolution of sustainability reporting in India

Regulations focusing on disclosure tend to have a domino effect on corporate sustainability as corporates need to begin by ensuring data availability, develop data collection methods, identify reporting gaps, develop new or modify existing practices to address these, benchmark performance versus past years and/or peers, and eventually develop a strategic approach to sustainability.

Additionally, it may not be enough to focus on sustainability within operational boundaries, as there is also growing demand to engage with supply chains. SEBI’s recent approval of the BRSR Core narrows down reporting focus to 50 assured performance indicators, but expands scope to include transparency in the value chain of listed entities. Listed entities aside, now private and smaller enterprises are also indirectly subject to regulatory purview. .

Sattva’s Research and Insights

Sattva has been closely monitoring sustainability disclosure progress of India inc (see Business Responsibility and Sustainability Reporting (BRSR) for the past two financial years. To analyse the momentum of ESG disclosures, a sample of 101 companies were selected across diverse sectors from top 1000 companies by market capitalization. 115 ESG metrics under 67 larger indicators (based on essential indicators of the BRSR framework) were collected from publicly available reports (Integrated reports, Annual reports, BRSR and Sustainability reports) and review was based on the ‘availability’ of data and not actual performance of metrics. Therefore, while the analysis may not indicate actual performance, it serves as a proxy to understand shifting trends in corporate sustainability focus.

Our review shows regulatory push to be yielding strong positive results in data transparency.

- Expansion in reporting practices: According to the NSE, 19% of the top market cap companies have voluntarily filed their BRSR reports (April 13, 2023), with Chemical, NBFC and IT sector leading the pack. Within our sample, 65% of the companies have adopted BRSR reporting. Similarly, our sample also shows a strong preference for transition towards Integrated reporting, with a significant single year growth of 21% in the number of companies shifting from standalone reports towards combined reporting of financial and non financial information

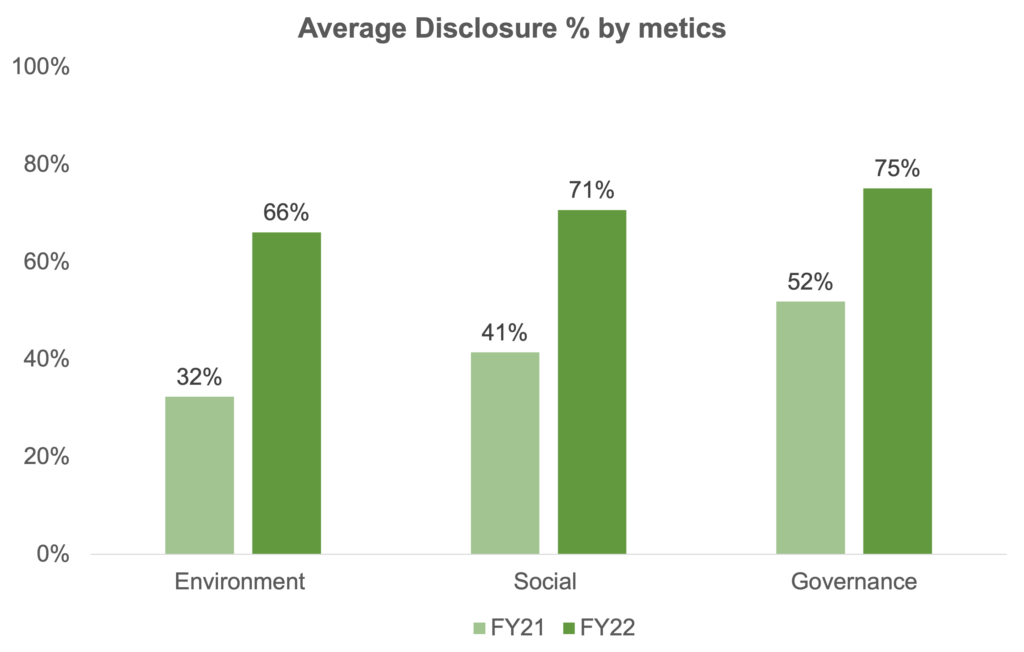

Significant growth in ESG disclosure rates: An average increase in disclosure of 29% was observed across ESG indicators between FY20-21 and FY21-22. Among these, environmental reporting has seen the most momentous increase with a 2x growth in average reporting. Average disclosure of social indicators increased by 30% and governance indicators showed a 23% increase on average.

Sattva’s Detailed insights

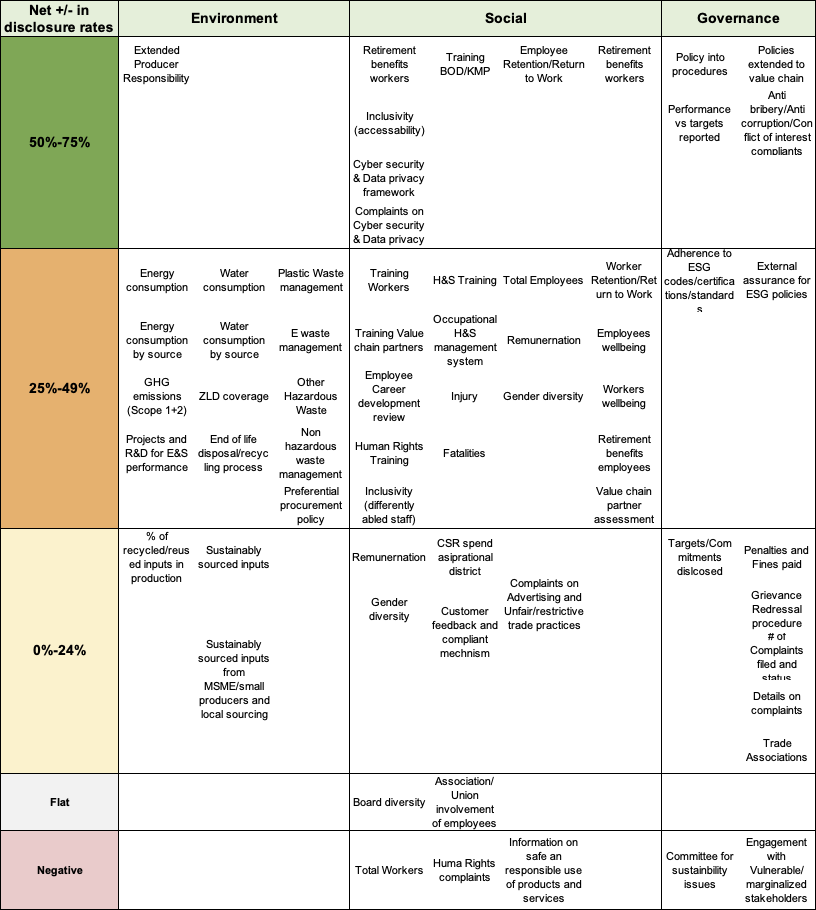

A closer look at the indicator level shows positive momentum overall, despite variances in increases.

- Some indicators demonstrate higher levels of reporting in FY21-22 versus other indicators that show lower growth, have remained flat or in some cases, declined. However, the lower growth, flat and decline reporting levels have a strong baseline level of reporting in FY 20-21 in the majority of the metrics and do not necessarily indicate lack of focus.

- Environmental indicators:

- In Energy & Emissions, reporting on energy consumption has increased by 28-38 percent and GHG reporting by 30 percent, highlighting the shifting focus of corporates to record and report this data. BRSR also requires reporting breakdown by source and in specific formats that could require additional capacity build.

- Water and Waste management indicators have also seen significant growth between 30-48%. A significant move in this regard is with disclosing if corporates have a Zero Liquid Discharge mechanism (48%).

- Extended Producer Responsibility has seen the maximum upward movement within Environmental indicators, with a 51% increase in reporting levels and relevant corporates disclosing if their waste management is in line with EPR plan submitted to Pollution Control Board. This consolidated approach to reporting under the BRSR has enhanced transparency on circularity efforts.

- Reporting on supply chain indicators, like sustainable sourced inputs, preferential procurement policy or sourcing from MSME/local procedures, also show significant positive trends. While there are already high levels of disclosure on sustainable sourcing policy, there has been a doubling of disclosure on the percentage of sustainably sourced inputs in our sample. Preferential procurement policy has also seen a significant 40 percent rise in disclosure from a mere 1 percent reporting in FY 20-21.

- Social indicators

- Diversity and inclusion: While reporting on diversity and inclusion was already high in the baseline year, reporting on equal opportunity employment for differently abled increased by 65 percent from the previous year

- Health and Safety: A 37 percent average increase in all metrics for Health and Safety reporting was observed. A 50 percent increase was seen in the reporting of the use of occupational health and safety management systems. >40 percent increase in injury and fatality rates was also noted along with a 28 percent increase in assessing value chain partners for human rights. This indicates the growing emphasis to execute, record and report on health and safety parameters from corporates.

- Human Rights: Reporting of Human rights training for employees and workers has increased considerably by 43 percent. A 29 percent increase in trainings for value chain partners on human rights, reflects the increasing focus on supply chain engagment

- Employee and Worker wellbeing: Reporting employee wellbeing metrics on insurance, retirement and other benefits was relatively high in the baseline year and saw a >30 percent increase in FY21-22. However, more significantly, there has been a major 47- 58% increase in reporting for worker wellbeing. This can be attributed directly to BRSR requiring detailed reporting for worker level information.

- Governance indicators

- ESG strategy: Metrics that provide insights on the organizations ESG strategy, (including establishing targets and commitments for sustainability, reporting performance against these targets converting policies to procedures) have also improved on disclosure reporting. Notably, a 64 percent increase was observed in reporting of conversion of policies to procedures and a 55 percent increase in performance versus targets. In line with the growing focus on sustainable value chain, there has also been a 63 percent increase in the reporting of whether policies also extend to supply chain members.

Complaints and Grievance redressal: While there has been no significant changes in reporting levels of penalties and fines paid and grievance redressal procedures, there has been a 30 percent increase in reporting on the details of the complaints. However, reporting on the complaints relating to anti bribery, anti corruption and conflict of interests has increased drastically by 51 percent in the FY21-22.

India Inc’s roadmap to a sustainable future

Preparedness is key to sustainable growth. While there is strong evidence of corporate adaptation to changing regulations, the preparedness for reporting and sustainability integration in the long term continues to be an area of focus. With regulatory interventions likely to continue, and global trends highly likely to intensify, there is an immediate need for corporates to develop a strategic approach to ESG rather than reactively adapting to compliance requirements.

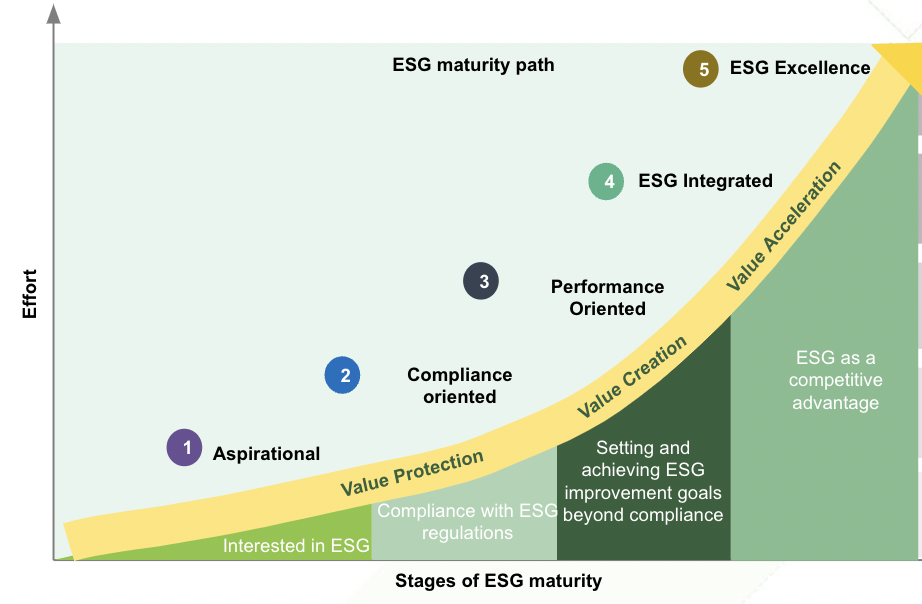

Corporates should begin by assessing their position on the ESG maturity path to determine their current position, future goals as well as resources required to achieve these goals.

- Aspirational: Companies that are not currently mandated by regulations but aspirational towards sustainable growth can leverage their position to prepare for future regulations, develop a basic ESG strategy based on their immediate stakeholders and differentiate themselves from other market players.

- Compliance oriented: Corporates directly impacted by regulations or with immediate need to adapt sustainable business practices, need to ensure agility in processes and continue to develop capabilities for adaptation.

- Performance oriented: Organizations already have a sustainability strategy in place and can seek to improve performance through diagnostics on their strategy, metrics, setting targets etc and benchmarking performance in the industry.

- ESG integrated: Corporates at higher levels of maturity can focus on creating longer term value by aligning their primary products and offerings to sustainability and investing in solutions to pivot business models.

ESG Excellence: Organisations aiming for ESG excellence should focus on paths to sector leadership, aim for transformations at sector level and across their value chain.

In the context of a rapidly changing environment and regulatory focus, an organization’s ability to transition towards strong compliance as well as higher levels of ESG maturity will have a lasting impact on their short and long term sustenance in the market. Riding this wave of opportunity can also enable organisations to generate financial, economic, and reputational value.

Sattva can enable corporates to transition along this maturity path, to know more about our offering and further details on our analysis please reach out to esg@sattva.co.in.

For detailed insights and data please download the attached deck.